Strategies

In the money (ITM) Covered Call

StrategiesA defensive theta setup where time decay matters more than a large price move.

Description

What matters most

The strategy uses 100 shares or ETF units plus a short ITM call. The main edge comes from the extrinsic value of the short call rather than from chasing a big directional move.

The strike should sit below the expected move of the cycle. In addition, the annualized return should be at least 20% to justify the capital usage.

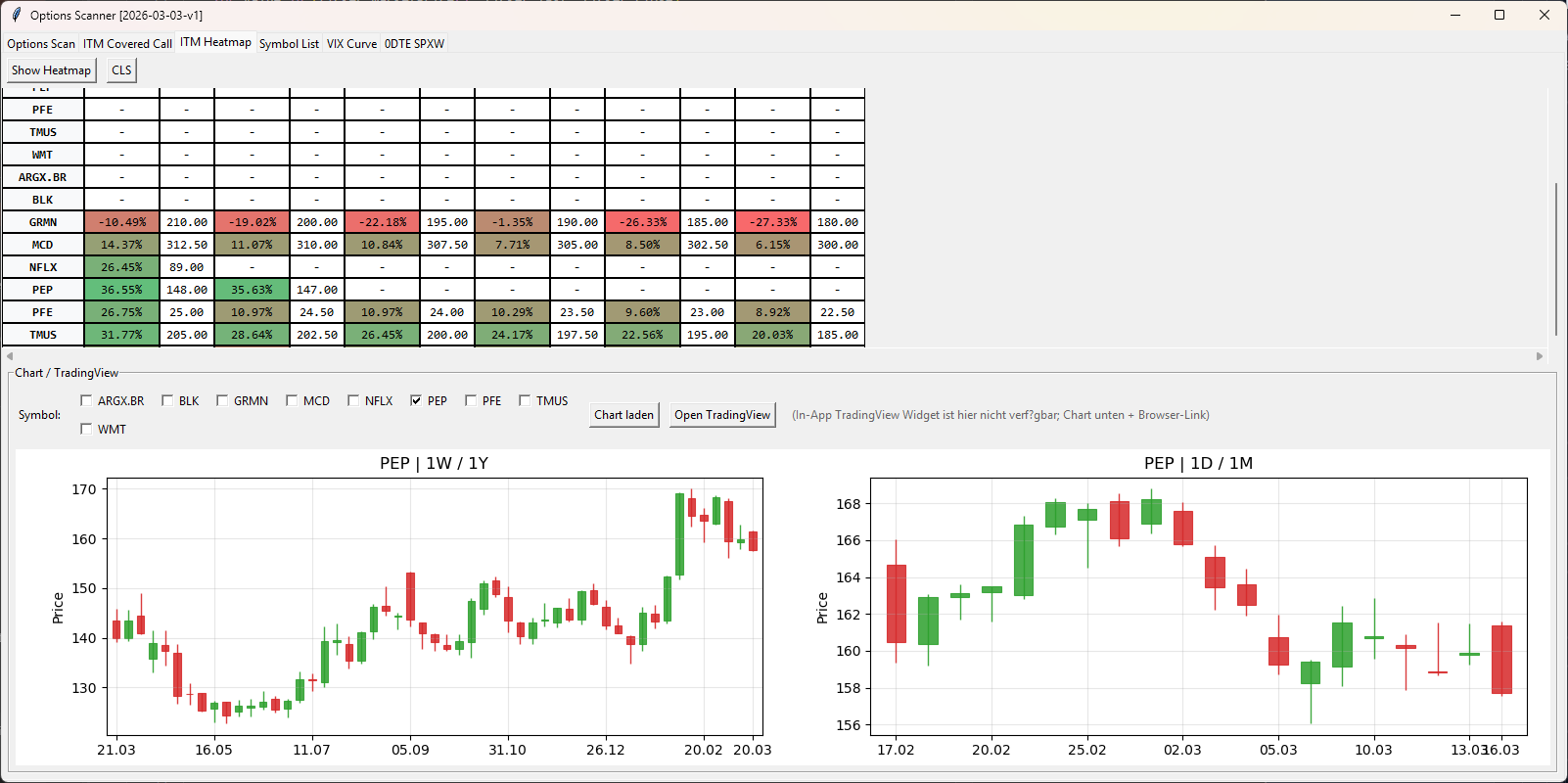

You can run a live scan for candidates in the OWS Tools.

One clear drawback is the missing upside. If the underlying rallies strongly, you do not meaningfully participate in that extra move because the short call caps the gain.

If the stock drops hard and ends below the strike into expiration, you can roll, sell the stock, or use an earlier active exit such as a stop around 10% in the underlying.

Alternative: Poor Man's Covered Call

Instead of buying 100 shares, you can use a long-dated call to gain the right to 100 shares and sell a shorter-dated call against it.

A common range is about 120 to 180 DTE and roughly 70 to 90 delta for the long call. That makes the structure much more capital-efficient and leaves more cash available for other trades.

Example: MSFT

- Spot 395.55 USD with 14 DTE and a 20 USD expected move.

- Strike Short call at 370 USD.

- Time value 28.00 minus 25.55 = 2.45 USD per share.

- Annualized About 11.9% per year on a strike basis, therefore below the 20% filter.

A scan for suitable stocks and ETFs can be run with the OWS tool. The included heatmap helps estimate whether a position is worth taking.

P/L Diagram

Schematic at expiration

Downside stays stock-like, while upside is capped once the call strike is reached.

Summary

Key points

- Thesis Theta and time decay are the real assumption.

- Strike ITM and below the expected move of the cycle.

- Return At least 20% annualized as a filter.

- Alternative Poor Man's Covered Call with a long-dated deep ITM call instead of 100 shares.

- Upside Strong rallies leave little additional participation.

- If it drops Roll, sell, or use an active stop around 10%.

- Scan Live scan via the OWS Tools.